U periodu 2007-2013. godina struktura zemalja uvoznica nije se bitnije promenila. Najveći deo uvoza Srbije dolazi iz Evrope. Pad ekonomske aktivnosti u Srbiji smanjio je tražnju za inostranom robom tako da je nakon krize značajno smanjen uvoz, što je uticalo na smanjenje trgovinskog deficita (sporiji rast uvoza od rasta izvoza).

U periodu 2007-2013. godina srpski uvoz beleži kontinuirani rast (naročito nakon krizne 2009. godine). Posmatrano prema geografskim zonama u posmatranom periodu preko 80% uvoza dolazi sa evropskog kontinenta. Ipak, udeo uvoza sa evropskog kontinenta se smanjuje, ali kontinuirano raste udeo uvoza iz zemalja EU, preko 60% u svim godinama (76,6% u 2013. godini). Oko 25% uvoza dolazi iz susednih zemalja, dok je uvoz iz bivših jugoslovenskih republika u opadanju (sa 14,2% i 11,6%). Pri tome, oko 50% uvoza iz zemalja van EU (ostatak Evrope) odnosi se na Rusiju. Inače, iz Rusije Srbija uvozi uglavnom energente i to u udelu između 11 i 16% ukupnog uvoza u posmatranim godinama. Pored energenata, Srbija uvozi reprodukcioni materijal (namenjen za proizvodnju i izvoz). Na smanjenje uvoza delom je uticala i depresijacija dinara, ali i smanjenje realnih zarada.

U posmatranom periodu nije se značajnije promenila struktura uvoza po geogradskim zonama. Udeo uvoza na evropska tržišta smanjen je sa 83,2% iz 2007. godine na 80,7% u 2013. godini, dok je povećan sa azijskog kontinenta sa 12,7% na 16% u posmatranim godinama. Ostala tržišta beleže smanjenje udela u uvozu: udeo sa američkog tržišta smanjen je sa 3,5% na 2,6%, dok je sa afričkog i pacifičkog tržišta, ionako mali po obimu i vrednosti, dodatno smanjen.

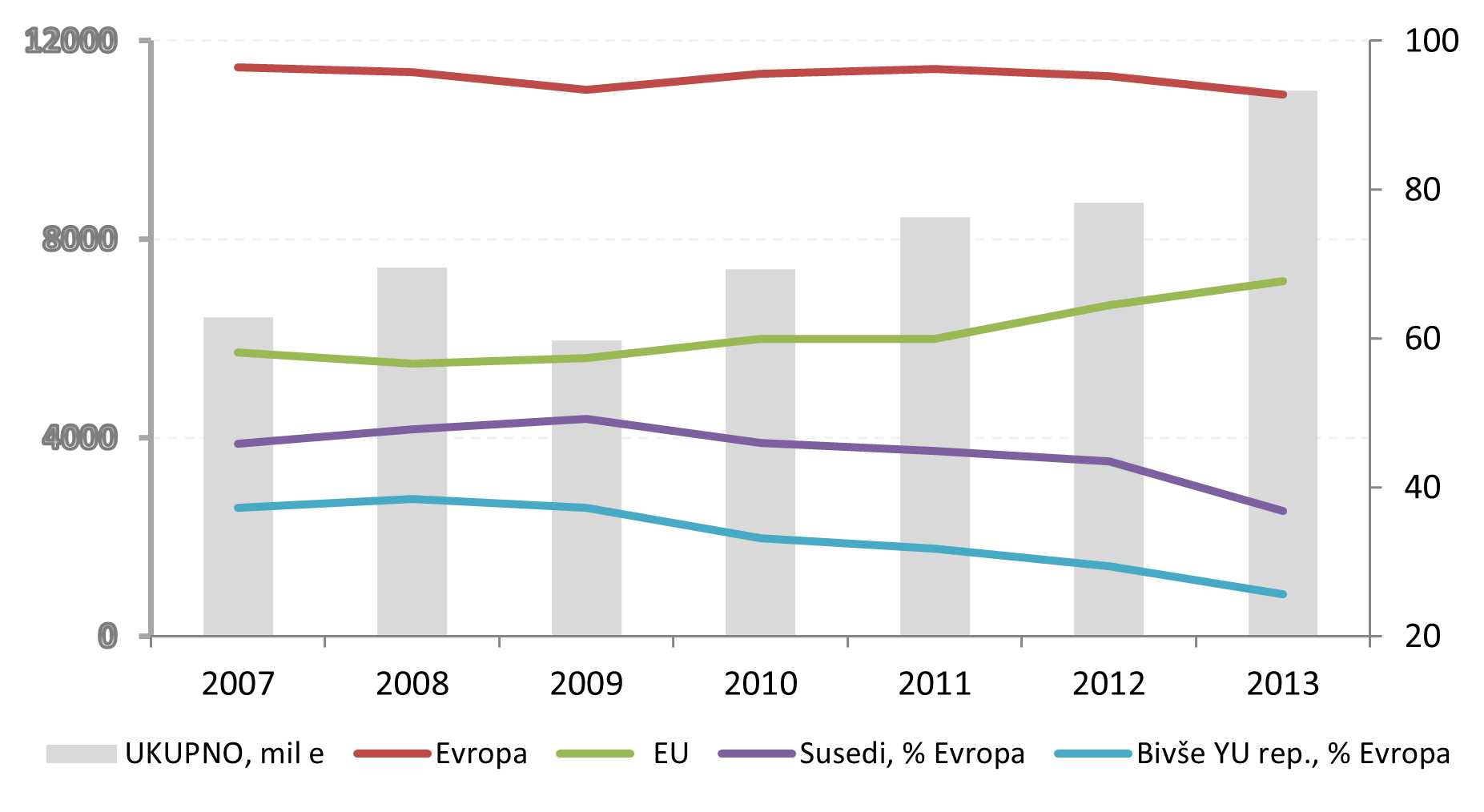

Napomena: EU = EU-27 (2013. EU-28); Susedi: Mađarska, Rumunija, Bugarska, Hrvatska (prvo polugodište), Bosna i Hercegovina, Crna Gora i Republika Makedonija; Bivše YU republike: Slovenija, Hrvatska, Bosna i Hercegovina, Crna Gora i Republika Makedonija.

Almost the entire volume of Serbian exports has traditionally been directed to European markets. In recent years, the decline in economic activity in these countries has not had a positive effect on export demand for domestic (Serbian) products. Positive effects on Serbia’s economic growth can be expected only through the redirection of exports toward expanding markets and through the diversification of the export product range.

During the period 2007–2013, Serbian exports recorded continuous growth, particularly after the crisis year of 2009. Observed by geographical zones, more than 90% of exports during the period were directed to the European continent. This raises a legitimate question as to whether such export concentration represents one of the causes of slow economic growth (and even decline in certain years) in Serbia, given the fact that Europe has recorded declining economic activity for several years, with some economies remaining in recession for prolonged periods.

More than 50% of Serbian exports to Europe are directed to EU countries (62.8% in 2013, following Croatia’s accession to the EU). An additional problem is that over 40% of total exports to Europe are realized in neighboring countries (with the exception of 2013, when the share was 37%). This indicates that the remainder of exports outside the EU is largely directed toward neighboring economies (up to 50%, except in 2013) or the former Yugoslav republics (over 30%, except in 2013). Furthermore, when taking into account that exports to the rest of Europe, i.e. non-EU countries, largely refer to the Russian market (between 10% and 24% in the observed years), it becomes evident that Serbia’s export assortment is very limited. A focus on stagnating markets (certain EU economies) or markets with low absorptive capacity (neighboring economies) cannot guarantee faster economic growth for Serbia.

Only from 2011 onward did the share of Serbian exports to the European continent begin to decline, accompanied by an increase in exports to EU member states, at the expense of a lower share of exports to neighboring countries and former Yugoslav republics (particularly in 2013). The share of exports to all other markets remained below 5%, which falls within the range of statistical insignificance. In other words, almost everything produced in Serbia was sold in Europe.

In 2013, the geographical structure of exports changed compared to previous years. The share of exports to European markets declined to 92.8%, while the share of exports to other continents increased to 7.2% (rising to 3.8% in the American continent, remaining at 2.5% in Asia, increasing to 0.1% in Oceania, and slightly declining to 0.8% in Africa). The largest contribution to the high export growth in 2013 (25.8%) came from passenger car exports, which exceeded EUR 1.5 billion compared to 2012.

Note: EU = EU-27 (EU-28 as of 2013); Neighbors: Hungary, Romania, Bulgaria, Croatia (first half of the year), Bosnia and Herzegovina, Montenegro, and the Republic of North Macedonia; Former Yugoslav republics: Slovenia, Croatia, Bosnia and Herzegovina, Montenegro, and the Republic of North Macedonia.