Dugi niz godina cena energenata nije remetila razvijene ekonomije, jer su industrije bile dovoljno fleksibilne da amortizuju rast cene energije. Poslednje dve godine one pokazuju nemoć usled divljanja cena energije i hrane.

Industrijska proizvodnja razvijenih ekonomija obično je rasla čak i sa višim cenama energije. To znači da je efekat povećanja cena bio skroman u poređenju sa efektima drugih promena u okruženju. Postojali su izuzeci, u energetski intenzivnim industrijama sa ograničenim mogućnostima zamene. Dramatične eksternalije dolazile su sa krizom ili u uslovima ranjivosti tržišta. Sa ukrajinskom krizom i obostranim sankcijama sa Ruskom federacijom došlo je do brojnih problema, i počeli su: da izostaju jeftini energenti, ugalj i sirovine iz Rusije; da pristiže skupa nafta i gas is SAD; da kasne retke sirovine iz Kine i drugih zemalja bogatih sirovinama.

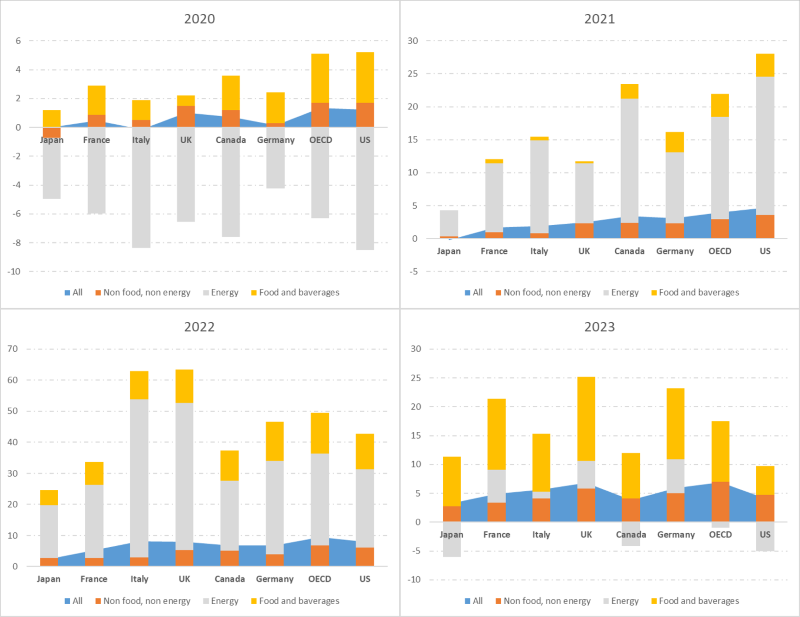

Rast cene energenata, usled neravnoteže ponude i potražnje na tržištu roba, uticale su na rast ukupne inflacije zemalja G7. Kvantitativne olakšice tokom Kovid-19 pandemije povećavale su likvidnost finansijskog sektora, a realni sektor nije osećao inflaciju. Investiciona apstinencija, niža sklonost ka ličnoj potrošnji, gomilanja novca, energetska kriza, neelastično tržište poljoprivrednih proizvoda ukazivali su na nadolazeće probleme. Tržište je reagovalo! Prvo se pojavila inflacija tražnje (2020), koja se potom prelila u inflaciju troškova (2021). Poslednja se kvalifikuje kao porast troškova proizvodnje – npr. podizanje zarada koje ne prati produktivnost rada utiče na rast cena. Konačno, došlo je do strukturne inflacije u kojoj privrede (2022) ne uspevaju da rastuće troškove proizvodnje prilagode cenama koje „divljaju“. Ulogu podstrekača inflacije preuzima cena hrane, u koju biva ukalkulisana ranije visoka cena energenata i nestašica sirovina. Cene hrane i bezalkoholnih pića nastavljaju da rastu i tokom 2023. godine, kao posledice naraslih troškova proizvodnje, uz manji pritisak cene energenata (osim u zemljama EU).

Globalni tokovi u periodu 2020-2023. godina pokazali su značajnu ulogu cene energenata u formiranju opšteg nivoa cena ili inflacije G7 zemalja. U periodu 2020-2022. godina inflacija je vođena cenama energenata, usled rastuće neravnoteže na tržištu nafte, cena naftnih fjučersa na finansijskom tržištu, kao i cena transporta nafte i osiguranje transporta. Međutim, bazna inflacija i cene hrane i bezalkoholnih pića su značajno doprinele da se inflacija ubrza tokom 2022. i 2023. godine. Cena bez hrane i energenata (bazna inflacija) uglavnom je stabilna, ali povišena. Ona je visoka i u svim razvijenim zemljama EU – u Nemačkoj iznad 5% (veća za 1 procentni poen u odnosu na 2022. godinu), u Francuskoj 4,2% (veća za 1,2 procentna poena), u Italiji 3,4% (veća za 0,6 procentnih poena). Još 12 zemalja OECD-a beleže rast bazne inflacije u ovom periodu (SAD 4,8%, VB 5,8%). Na visoke cene hrane i bezalkoholnih pića delom su uticale ranije ukalkulisane cena energenata, ali i rastući troškovi u lancu snabdevanja (cene, marže, sirovine, penali, osiguranje).

Izvor: OECD baza podataka

For many years, the price of energy did not disturb developed economies, because the industries were flexible enough to amortize the increase in the energy price. In the last two years, they have shown weakness due to the rampant energy and food prices.

Industrial production in advanced economies has typically grown even with higher energy prices. This means that the effect of the price increase was modest compared to the effects of other environmental changes. There were exceptions in energy-intensive industries with limited substitution possibilities. Dramatic externalities come with a crisis or conditions of market vulnerability. With the Ukrainian crisis and mutual sanctions with the Russian Federation, several problems arose, and they started: the absence of cheap energy, coal, and raw materials from Russia; that expensive oil and gas arrive from the USA; that late rare raw materials from China and other countries rich in raw materials.

The increase in energy prices, due to the supply and demand imbalance in the goods market, influenced the growth of the overall inflation of the G7 countries. Quantitative easing during the COVID-19 pandemic increased the financial sector liquidity, while the real sector did not feel such inflationary pressure. Investment abstinence, lower propensity for personal consumption, hoarding of money, energy crisis, and inelastic market of agricultural products pointed to upcoming problems. The market reacted! First, there was demand inflation (2020), which then spilled over into cost inflation (2021). The latter qualifies as an increase in production costs – e. g. raising wages that do not keep up with labor productivity affects price growth. Finally, there was structural inflation where economies (2022) failed to match rising production costs with „runaway“ prices. The role of the instigator of inflation is taken over by the price of food, which includes the previously high price of energy and the shortage of raw materials. Food and soft drink prices continued to rise during 2023, which increased production costs, with less pressure on energy prices (except in EU countries).

Global flows in the period 2020-2023. years showed a significant role in energy prices in the general price level or inflation of the G7 countries. In the period 2020-2022. inflation is driven by energy prices, due to the growing imbalance in the oil market, the price of oil futures on the financial market, and the price of oil transportation and transportation insurance. However, core inflation and food and soft drink prices have accelerated inflation in 2022 and 2023. The price without food and energy (core inflation) was mostly stable, but elevated. It is also high in all developed EU countries – in Germany above 5% (1 percentage point higher than in 2022), in France 4.2% (1.2 percentage points higher), in Italy 3.4% (higher by 0.6 percentage points). Another 12 OECD countries recorded an increase in core inflation in this period (USA 4.8%, UK 5.8%). The high prices of food and non-alcoholic beverages were partly influenced by previously calculated energy prices and the growth of costs in the supply chain (prices, margins, raw materials, penalties, insurance).

Source: OECD database