Od 2000. godine, srpska ekonomija je prošla kroz duboku strukturnu transformaciju – od ekonomije kojom dominira realni sektor do ekonomije bez jasnog proizvodnog jezgra. Udeo ključnih sektora kao što su proizvodnja, poljoprivreda i javni sektor pao je sa 60,8% na 33,3% bruto dodate vrednosti, dok nijedan sektor danas ne pruža snažnu i stabilnu osnovu za rast. Rezultat je ekonomija koja sve više zavisi od spoljnih izvora rasta, sa ograničenim unutrašnjim kapacitetom za održivi razvoj.

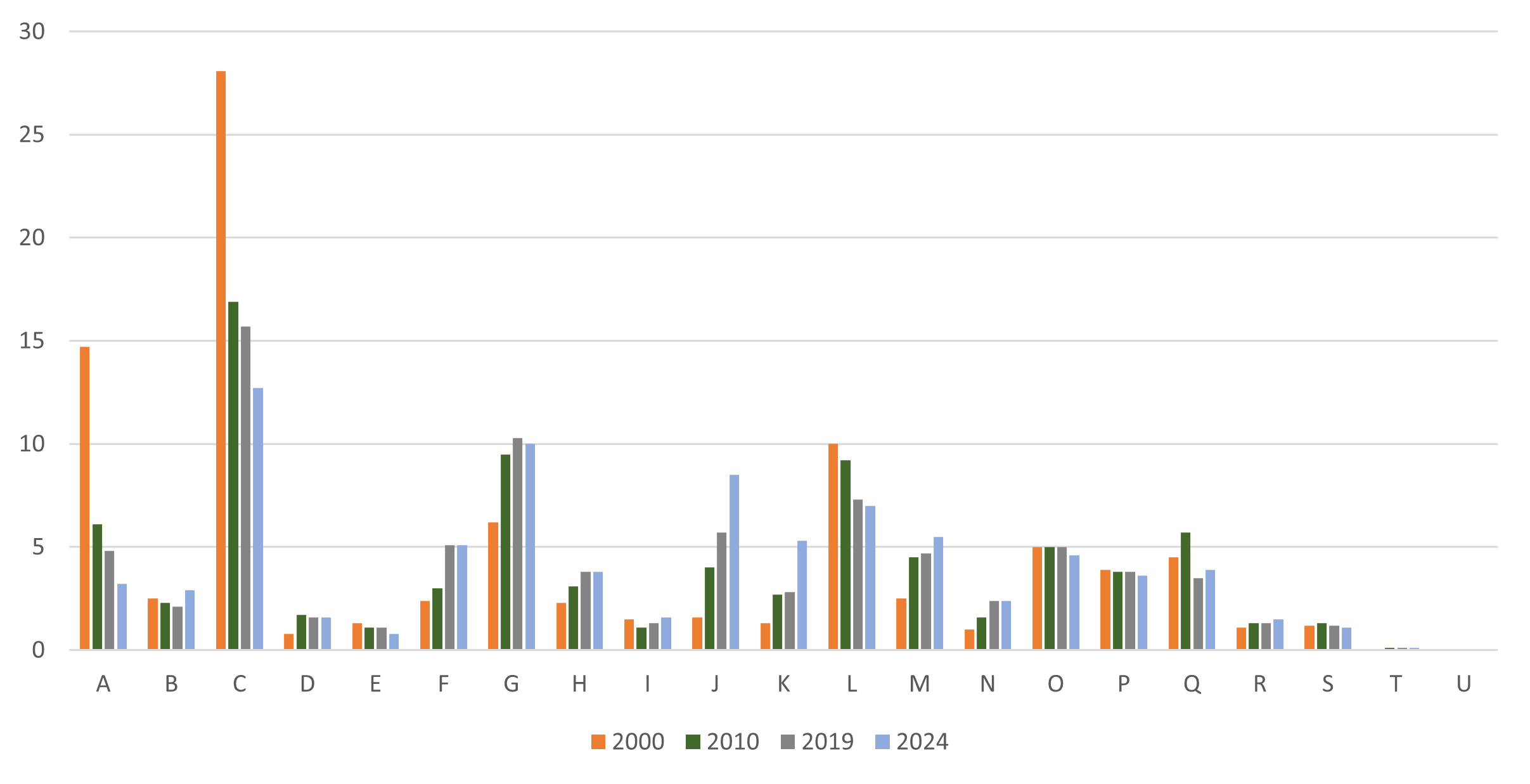

Kako izgleda struktura srpske ekonomije danas i kako se upoređuje sa 2000. godinom? U 2024. godini, ekonomiju karakteriše fragmentirana raspodela bruto dodate vrednosti: proizvodnja čini 12,7%, veleprodaja i maloprodaja 10%, dok većina ostalih sektora pojedinačno ostaje ispod 10%, uključujući informisanje i komunikacije sa 8,5%, pri čemu su strateški sektori kao što su energetika (D) i vodoprivreda (E) uglavnom marginalizovani. Nasuprot tome, 2000. godine ekonomija je imala jasnu strukturnu okosnicu: proizvodni sektor (BCDE) činio je 32,7%, poljoprivreda 14,7%, a javni sektor (OPQ) 13,4%, dok je uslužni sektor (GHI) iznosio 10%. Danas, odsustvo dominantnog sektora odražava nedostatak specijalizacije, nedovoljan fokus investicija i slabu konkurentnost.

U mnogim uspešnim ekonomijama, strukturna transformacija je značila postepeno prebacivanje sa poljoprivrede i proizvodnje ka sektorima usluga sa višom dodatom vrednošću, komunikacijama i finansijama. Međutim, ova tranzicija zahteva snažan rast produktivnosti i tehnološku nadogradnju. U Srbiji ovaj proces nije završen. Umesto da se tradicionalni sektori zamene konkurentnim modernim, ekonomija je postala strukturno razblažena — bez jasnog motora rasta.

Zašto se to dogodilo? Odgovor leži u modelu razvoja. Brza liberalizacija, neefikasna privatizacija i odsustvo koherentnog okvira za finansiranje razvoja doveli su do slabljenja ključnih sektora, posebno poljoprivrede i proizvodnje. Istovremeno, nedovoljna pažnja nije posvećena obrazovanju i dugoročnoj izgradnji kapaciteta. To ne bi bilo problematično da su se pojavili novi konkurentni sektori koji bi zamenili stare. Međutim, to se nije dogodilo. Kao rezultat toga, ekonomski rast je ostao nestabilan, a produžena stagnacija tokom 2008-2017. godine potvrdila je postojanje dubljih strukturnih problema.

Prirodu problema dodatno otkrivaju obrasci investicija. Iako su nominalne investicije bile značajne, one su bile koncentrisane u sektorima kao što su stručne i naučne delatnosti (MN), usluge (GHI), umetnost i rekreacija (RST), javna uprava (OPK), proizvodnja (BCDE) i IKT (JK). Međutim, sam obim investicija ne garantuje rast produktivnosti. U mnogim slučajevima, ove investicije nisu se pretvorile u veću efikasnost ili jaču konkurentnost, što ukazuje na strukturne neefikasnosti unutar ekonomije.

Savremeni modeli razvoja sve više se oslanjaju na interakciju između tehnologije, inovacija i ljudskog kapitala. Samo ulaganje u tehnologiju nije dovoljno ako ga ne prati paralelno povećanje ljudskog kapitala. Tehnološka infrastruktura bez kvalifikovane radne snage ostaje nedovoljno iskorišćena. U Srbiji je ova neravnoteža jasno vidljiva. Dok se udeo tehnološki naprednih sektora vremenom povećavao, dostigavši 11% u 2024. godini, ulaganja u obrazovanje su ostala stalno niska. Udeo obrazovanja u bruto dodatoj vrednosti ostao je ispod 4%, a dodatno je opao na 3,6% u 2024. godini.

Kašnjenje od 25 godina u strukturnom prilagođavanju efikasno predstavlja kašnjenje cele tehnološke generacije. Ovaj jaz objašnjava zašto Srbija i dalje zaostaje za razvijenijim ekonomijama. Bez jasnog strukturnog jezgra, snažnijih ulaganja u ljudski kapital i prelaska na rast vođen produktivnošću, ekonomija rizikuje da ostane fragmentirana i zavisna, umesto da konvergira ka višim nivoima razvoja.

Izvor: RZS

Napomena 1: učešće u bruto dodatoj vrednosti

Napomena 2: Sektori privrede: A – Poljoprivreda, šumarstvo i ribarstvo B – Rudarstvo C – Prerada u industriji D – Snabdevanje električnom energijom, gasom, parom i klimatizacijom E – Snabdevanje vodom; upravljanje otpadnim vodama, kontrola procesa uklanjanja otpada i slične aktivnosti F – Građevinarstvo G – Trgovina na veliko i malo; popravka motornih vozila i motocikala H – Saobraćaj i skladištenje I – Usluge smeštaja i ugostiteljstva J – Informacije i komunikacije K – Finansijske i osiguravajuće aktivnosti L – Poslovanje sa nekretninama M – Stručne, naučne i tehničke aktivnosti N – Administrativne i pomoćne uslužne delatnosti O – Državna uprava i odbrana; obavezno socijalno osiguranje P – Obrazovanje K – Zdravstvo i socijalna zaštita R – Umetnost; zabava i rekreacija S – Ostale uslužne delatnosti T – Delatnost domaćinstva kao poslodavca; delatnost domaćinstava koja proizvode robu i usluge za sopstvene potrebe U – Delatnost eksteritorijalnih organizacija i tela

Since 2000, the Serbian economy has undergone a profound structural transformation – from an economy dominated by the real sector to one without a clear production core. The share of key sectors such as manufacturing, agriculture and the public sector has fallen from 60.8% to 33.3% of gross value added, while no single sector today provides a strong and stable foundation for growth. The result is an economy increasingly dependent on external sources of growth, with limited internal capacity for sustainable development.

What does the structure of the Serbian economy look like today, and how does it compare to 2000? In 2024, the economy is characterized by a fragmented distribution of gross value added: manufacturing accounts for 12.7%, wholesale and retail trade 10%, while most other sectors individually remain below 10%, including information and communications at 8.5%, with strategic sectors such as energy (D) and water (E) largely marginalized. In contrast, in 2000 the economy had a clear structural backbone: the manufacturing sector (BCDE) accounted for 32.7%, agriculture 14.7%, and the public sector (OPQ) 13.4%, while services (GHI) stood at 10%. Today, the absence of a dominant sector reflects a lack of specialization, insufficient investment focus and weak competitiveness.

In many successful economies, structural transformation has meant a gradual shift from agriculture and manufacturing toward higher value-added services, communication and financial sectors. However, this transition requires strong productivity growth and technological upgrading. In Serbia, this process has not been completed. Instead of replacing traditional sectors with competitive modern ones, the economy has become structurally diluted – without a clear engine of growth.

Why did this happen? The answer lies in the development model. Rapid liberalization, ineffective privatization and the absence of a coherent development financing framework led to the weakening of key sectors, particularly agriculture and manufacturing. At the same time, insufficient attention was given to education and long-term capacity building. This would not have been problematic if new competitive sectors had emerged to replace the old ones. However, this did not occur. As a result, economic growth remained volatile, and the prolonged stagnation during 2008-2017 confirmed the existence of deeper structural problems.

The nature of the problem is further revealed by investment patterns. Although nominal investments have been significant, they have been concentrated in sectors such as professional and scientific activities (MN), services (GHI), arts and recreation (RST), public administration (OPQ), manufacturing (BCDE) and ICT (JK). However, the volume of investment alone does not guarantee productivity growth. In many cases, these investments have not translated into higher efficiency or stronger competitiveness, indicating structural inefficiencies within the economy.

Modern development models increasingly rely on the interaction between technology, innovation and human capital. Investment in technology alone is not sufficient if it is not accompanied by a parallel increase in human capital. Technological infrastructure without skilled labor remains underutilized. In Serbia, this imbalance is clearly visible. While the share of technologically advanced sectors has increased over time, reaching 11% in 2024, investment in education has remained persistently low. The share of education in gross value added has stayed below 4%, declining further to 3.6% in 2024.

A delay of 25 years in structural adjustment effectively represents a delay of an entire technological generation. This gap explains why Serbia continues to lag behind more developed economies. Without a clear structural core, stronger investment in human capital and a shift toward productivity-driven growth, the economy risks remaining fragmented and dependent, rather than converging toward higher levels of development.

Source: RZS

Note 1: share in gross value added

Note 2: Sectors of the economy: A – Agriculture, forestry and fishing B – Mining C – Processing to industry D – Supply of electricity, gas, steam and air conditioning E – Supply of water; waste water management, control of waste removal processes and similar activities F – Construction G – Wholesale and retail trade; repair of motor vehicles and motorcycles H – Transportation and storage I – Accommodation and catering services J – Information and communications K – Financial and insurance activities L – Real estate business M – Professional, scientific and technical activities N – Administrative and auxiliary service activities O – State administration and defense; compulsory social insurance P – Education K – Health and social protection R – Art; entertainment and recreation S – Other service activities T – Activity of the household as an employer; activity of households that produce goods and services for their own needs U – Activity of extraterritorial organizations and bodies