Pad globalnog tržišta u SAD početkom avgusta nije iznenađenje. Problemi na tržištu rada ali i na tržištu hartija od vrednosti povećavaju strah od recesije do kraja 2024. godine, nakon Fed-ovog snažnog čina da obuzda inflaciju povećanjem stopa. Ako ostane inverzna kriva prinosa, privreda SAD će upasti u recesiju do kraja godine.

Finansijska tržišta pokazuju da strah od recesije nije slučajan. Investitori gube poverenje u privredu, očigledno zbog negativnih kratkoročnih kretanja u privredi. Inverzna kriva prinosa to potvrđuje, jer se finansijsko tržište suočava sa većim prinosima na kratkoročna ulaganja u prvoj polovini 2024. godine.

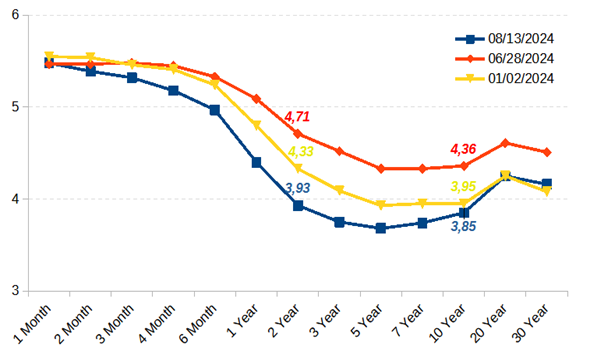

Kriva prinosa (Slika) pokazuje odnos državnih obveznica različitih rokova dospeća. Kako su prinosi između desetogodišnjih i dvogodišnjih državnih obveznica u korist poslednjih (za sva tri datuma) radi se o obrnutoj krivi prinosa. Tako je od jula 2022. godine, što je duži period od ranije najdužeg perioda između inverzije i početka recesije od oko 1,5 godina.

Avgustovska kriva prinosa je relativno povoljnija, kada se porede državne obveznice sa dve godine dospeća i one sa dvadest i trideset godina dospeća. Mnogi smatraju da je ovaj indikator sve manje pouzdan. Očigledno je da je meko sletanje daleko prikladnije za javnost od crnih prognoza finansijskog tržišta. Kako god bolje zvučalo, politika kamatnih stopa mora biti izbalansirana kako bi se istovremno postigla stimulacija privrede i borba protiv inflacije.

I to nije sve! Još jedan reprezentativni pokazatelj signalizira na anomalije ekonomije i potencijalnu recesiju, a to je indikator Sahmovog pravila je 0.53 procentnih poena (tromesečni pokretni prosek stope nezaposlenosti je iznad najnižeg tromesečnog pokretnog proseka u protekloj godini). Sve ovo navelo je početkom avgusta J.P.Morgan da poveća predviđene šanse za recesiju u SAD pre kraja godine na 35% (sa 25%). Porazne su i prognoze FED-a Nev Iork, koje ističu da se recesija može očekivati sa verovatnoćom od 56% (na bazi raspona prinosa između kamatnih stopa kratkoročnih i dugoročnih državnih obveznica SAD).

Izvor: https://statista.com, https://newyorkfed, https://jpmorganchase.com

Napomena: Trezor je napustio metodu kvazi-kubičnog hermitskog splajna (HS) za konstrukciju krive prinosa, koja direktno koristi prinose na sekundarnom tržištu kao ulazne podatke za kreiranje krive prinosa za koju se pretpostavlja da je parna kriva. Nova metoda je Monotona konveksna (MC), koja počinje tako što se cene na sekundarnom tržištu pretvaraju u prinose i koriste za podizanje trenutnih terminskih stopa na ulaznim tačkama dospeća, tako da se cene ovih instrumenata sekvencijalno određuju bez greške. Krive prinosa se od početka decembra 2021. godine obračunavaju od stopa proizvedenih obe metode.

The decline of the global market in the US at the beginning of August is not a surprise. Problems in the labor market as well as in the securities market increase the fear of a recession by the end of 2024, after a strong act by the Fed to curb inflation by raising rates. If the inverted yield curve remains, the US economy will fall into recession by the end of the year.

Financial markets are showing that the fear of recession is not accidental. Investors are losing confidence in the economy, apparently due to negative short-term developments in the economy. The inverse yield curve confirms this, as the financial market faces higher returns on short-term investments in the first half of 2024.

The yield curve (picture) shows the ratio of government bonds of different maturities. Since the yields between the ten-year and two-year government bonds favor the latter (for all three dates), it is an inverted yield curve. This has been the case since July 2022, which is a longer period than the previous longest period between the inversion and the beginning of the recession of about 1.5 years.

The August yield curve is relatively more favorable when comparing government bonds with maturities of two years and those with maturities of twenty and thirty years. Many consider this indicator to be less and less reliable. Obviously, a soft landing is much more appropriate for the public than financial market doomsday forecasts. No matter how better it sounds, the policy of interest rates must be balanced in order to simultaneously achieve the stimulation of the economy and the fight against inflation.

And that’s not all! Another representative indicator signals the anomalies of the economy and a potential recession, which is the indicator of Sahm’s rule 0.53 percentage points (the three-month moving average of the unemployment rate is above the lowest three-month moving average of the past year). All this encouraged J.P. Morgan at the beginning of August to increase its predicted chances of a recession in the US before the end of the year to 35% (from 25%). The forecasts of the New York FED are also devastating, pointing out that a recession can be expected with a probability of 56 percent (based on the yield range between the interest rates of short-term and long-term US government bonds).

Source: https://statista.com, https://newyorkfed, https://jpmorganchase.com

Note: Treasury has abandoned the quasi-cubic Hermitian spline (HS) method for yield curve construction, which directly uses secondary market yields as input to create a yield curve that is assumed to be an even curve. The new method is Monotone Convex (MC), which starts by converting secondary market prices into yields and using them to raise current forward rates at maturity entry points, so that these instruments are sequentially priced without error. The yield curves are calculated as of the beginning of December 2021 based on the rates produced by both methods.