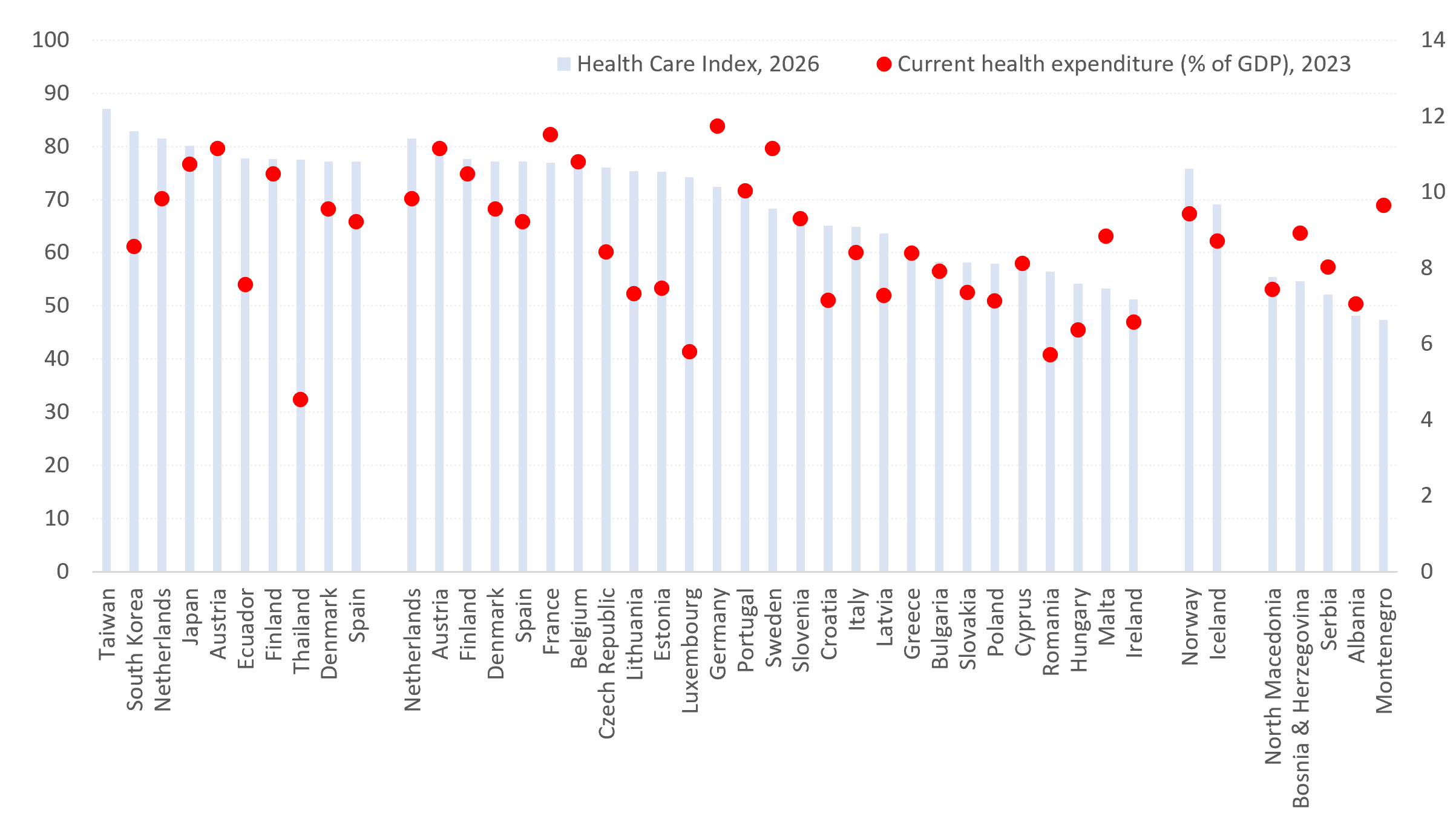

Kvalitet i dostupnost zdravstvene zaštite nisu samo pokazatelji društvenog blagostanja, već i važni determinanti ekonomskih performansi. Zemlje sa kvalitetnijim zdravstvenim sistemima uglavnom ostvaruju veću produktivnost, duži radni vek stanovništva, snažniji ljudski kapital i veću otpornost na demografske i ekonomske šokove. Prema najnovijem Indeksu zdravstvene zaštite (Healthcare Index), najbolje rangirani zdravstveni sistemi na svetu nalaze se na Tajvanu (87,1), u Južnoj Koreji (82,9), Holandiji (81,5), Japanu (80,1) i Austriji (78,9). U okviru Evropske unije prednjači Holandija, dok se Srbija (52,1) nalazi ispod svih država članica EU i većine zemalja iz okruženja. Istovremeno, Srbija za zdravstvo izdvaja 8,0% BDP-a, što je više od pojedinih zemalja EU koje ostvaruju bolje zdravstvene rezultate, što ukazuje da izazov nije samo nivo izdvajanja, već i efikasnost upravljanja zdravstvenim sistemom i raspodele resursa.

Zdravstvo se sve više posmatra kao produktivna investicija, a ne kao socijalni trošak. Savremene teorije ekonomskog rasta, posebno one zasnovane na ljudskom kapitalu, naglašavaju da zdravije stanovništvo direktno doprinosi ekonomskom rastu kroz veću produktivnost rada, manje odsustvovanje sa posla, duže učešće na tržištu rada i snažniji inovacioni potencijal. U tom smislu, zdravstveni sistemi predstavljaju deo ekonomske infrastrukture jedne zemlje, na isti način kao transportna, energetska ili digitalna infrastruktura.

Indeks zdravstvene zaštite meri percepciju građana o kvalitetu zdravstvenih sistema kroz više dimenzija, uključujući stručnost zdravstvenog osoblja, dostupnost medicinskih usluga, opremljenost sistema, brzinu reagovanja, vreme čekanja, troškove i ukupno poverenje u zdravstvene institucije. Zbog toga ovaj indeks predstavlja koristan pokazatelj efikasnosti pretvaranja finansijskih resursa u zdravstvene rezultate.

Na globalnom nivou dominiraju ekonomije Istočne Azije. Tajvan (87,1) zauzima prvo mesto, a slede Južna Koreja (82,9) i Japan (80,1). Ove zemlje kombinuju široku pokrivenost zdravstvenim uslugama, napredne medicinske tehnologije, snažne sisteme preventivne zaštite i visoko obrazovane zdravstvene radnike. Istovremeno, reč je o ekonomijama koje karakterišu velika ulaganja u obrazovanje, istraživanje, inovacije i tehnološki razvoj.

U Evropskoj uniji najviše rangirani zdravstveni sistemi nalaze se u Holandiji (81,5), Austriji (78,9), Finskoj (77,6), Danskoj (77,2), Španiji (77,2) i Francuskoj (77,0). Njihov uspeh ne može se objasniti samo visinom zdravstvene potrošnje. Mnogo važnija je sposobnost da se finansijski resursi pretvore u dostupne, efikasne i pouzdane zdravstvene usluge.

Podaci o izdvajanjima za zdravstvo pružaju dodatnu perspektivu. Tokom 2023. godine tekuća zdravstvena potrošnja u EU u proseku je iznosila 10,0% BDP-a. Nemačka je izdvajala najveći udeo BDP-a za zdravstvo (11,7%), a sledile su Francuska (11,5%), Austrija (11,2%) i Švedska (11,2%). Na drugom kraju lestvice nalazile su se Luksemburg i Rumunija (5,7%), Mađarska (6,4%) i Irska (6,6%).

Odnos između izdvajanja i kvaliteta zdravstvenog sistema nije uvek linearan. Austrija kombinuje visoka izdvajanja za zdravstvo (11,2% BDP-a) sa jednim od najboljih zdravstvenih sistema u Evropi (78,9). Holandija ostvaruje najbolji rezultat u EU prema Indeksu zdravstvene zaštite (81,5), iako za zdravstvo izdvaja manji procenat BDP-a (9,8%) od Nemačke, Francuske, Austrije ili Švedske. Nemačka, sa druge strane, izdvaja 11,7% BDP-a za zdravstvo – među najvišim nivoima u svetu – ali se nalazi tek na 13. mestu među zemljama EU prema kvalitetu zdravstvene zaštite (72,4). To pokazuje da su institucionalni kvalitet, efikasnost upravljanja, preventivne politike, digitalizacija i organizacija zdravstvene radne snage jednako važni kao i nivo finansiranja.

Evropska slika pokazuje jasnu geografsku pravilnost. Zemlje severne i zapadne Evrope dominiraju i prema kvalitetu zdravstvene zaštite i prema zdravstvenim izdvajanjima, dok južne i istočne članice uglavnom ostvaruju slabije rezultate. Zemlje poput Rumunije (56,5), Mađarske (54,2), Malte (53,3) i Irske (51,2) nalaze se pri dnu rang-liste kvaliteta zdravstvene zaštite, uprkos različitim nivoima potrošnje.

Region Balkana i dalje značajno zaostaje za evropskim prosekom. Severna Makedonija (55,4) i Bosna i Hercegovina (54,6) ostvaruju nešto bolje rezultate od Srbije (52,1), dok Albanija (48,1) i Crna Gora (47,4) beleže najniže ocene kvaliteta zdravstvenih sistema. Pozicija Srbije je posebno zanimljiva jer izdvajanja za zdravstvo dostižu 8,0% BDP-a, što je više nego u Rumuniji (5,7%), Mađarskoj (6,4%), Hrvatskoj (7,1%), Poljskoj (7,1%), Litvaniji (7,3%), Estoniji (7,5%) i Bugarskoj (7,9%), dok je kvalitet zdravstvene zaštite i dalje relativno nizak.

To ukazuje da je izazov Srbije sve više pitanje efikasnosti, a ne isključivo finansiranja. Jaz između zdravstvene potrošnje i zdravstvenih rezultata odražava šire strukturne probleme povezane sa kvalitetom upravljanja, modernizacijom infrastrukture, organizacijom zdravstvenog sistema, demografskim pritiscima i zadržavanjem medicinskog kadra. Kontinuirani odlazak lekara, medicinskih sestara i visokokvalifikovanih zdravstvenih radnika smanjuje kapacitete sistema i povećava opterećenje preostalog osoblja, stvarajući začarani krug koji negativno utiče na kvalitet usluga i zadovoljstvo građana.

Posebno je značajna povezanost između kvaliteta zdravstvene zaštite i demografske održivosti. Zemlje sa razvijenijim zdravstvenim sistemima uglavnom ostvaruju duži životni vek, niže stope smrtnosti, bolje upravljanje hroničnim bolestima i veću otpornost na starenje stanovništva. Kako se Evropa suočava sa demografskim padom i nedostatkom radne snage, kvalitet zdravstvene zaštite sve više postaje faktor ekonomske konkurentnosti, a ne samo cilj socijalne politike.

Poređenje Srbije sa vodećim zemljama EU ukazuje na širi razvojni izazov. Razlika između Srbije (52,1) i Holandije (81,5) ili Austrije (78,9) ne može se objasniti samo nivoom dohotka ili veličinom zdravstvenog budžeta. Ona odražava i razlike u institucionalnim kapacitetima, efikasnosti ulaganja, preventivnim politikama, digitalizaciji, kvalitetu upravljanja i sposobnosti zadržavanja visokokvalifikovanih stručnjaka.

Pouka evropskih iskustava je jasna – najbolje zdravstvene sisteme nemaju nužno zemlje koje troše najviše, već one koje raspoloživa sredstva koriste najefikasnije. Zdravstvo nije budžetski trošak, već jedna od najvažnijih investicija koje država može da napravi. Zbog toga centralni izazov više nije samo povećanje izdvajanja, već unapređenje efikasnosti, upravljanja, zadržavanja ljudskog kapitala i institucionalnih performansi. Zemlje koje uspešno pretvaraju zdravstvenu potrošnju u zdravstvene rezultate grade ne samo zdravija društva, već i produktivnije, otpornije i konkurentnije ekonomije. Za Srbiju, zdravstvo stoga nije samo socijalno pitanje – ono sve više postaje pitanje dugoročne razvojne strategije.

Izvor: Numbeo; Baza Svetske banke

The quality of healthcare is not only a measure of social welfare but also a determinant of economic performance. Countries with better healthcare systems generally achieve higher productivity, longer working lives, stronger human capital, and greater resilience to demographic and economic shocks. According to the latest Healthcare Index, the world’s highest-ranked healthcare systems are found in Taiwan (87.1), South Korea (82.9), the Netherlands (81.5), Japan (80.1), and Austria (78.9). Within the EU, the Netherlands leads, while Serbia (52.1) ranks below all EU member states and most neighboring countries. At the same time, Serbia allocates 8.0% of GDP to healthcare, which is above several EU countries with better healthcare outcomes, suggesting that the challenge is not only the level of spending but also the efficiency of healthcare governance and resource allocation.

Healthcare is increasingly recognized as a productive investment rather than a social expenditure. Modern growth theories, particularly those focused on human capital, emphasize that healthier populations contribute directly to economic growth through higher labor productivity, lower absenteeism, longer participation in the labor market, and stronger innovative capacity. In this context, healthcare systems represent part of a country’s economic infrastructure in the same way that transport, energy, or digital networks do.

The Healthcare Index measures public perceptions of healthcare quality through multiple dimensions, including professional competence, availability of medical services, equipment, responsiveness, waiting times, costs, and overall confidence in healthcare institutions. The index therefore provides a useful proxy for evaluating how effectively healthcare systems translate financial resources into healthcare outcomes.

At the global level, East Asian economies dominate. Taiwan (87.1) occupies the leading position, followed by South Korea (82.9) and Japan (80.1). These countries combine broad healthcare coverage, advanced medical technologies, strong preventive care systems, and highly educated healthcare professionals. Importantly, they also belong to economies characterized by substantial investment in education, research, innovation, and technological development.

Within the European Union, the highest-ranked healthcare systems are found in the Netherlands (81.5), Austria (78.9), Finland (77.6), Denmark (77.2), Spain (77.2), and France (77.0). Their success cannot be explained solely by healthcare spending. Rather, it reflects the ability to convert financial resources into accessible, efficient, and trusted healthcare services.

Healthcare expenditure data provide an additional perspective. In 2023, current healthcare expenditure in the EU averaged 10.0% of GDP. Germany allocated the highest share of GDP to healthcare (11.7%), followed by France (11.5%), Austria (11.2%), and Sweden (11.2%). At the opposite end of the scale were Luxembourg and Romania (5.7%), Hungary (6.4%), and Ireland (6.6%).

The relationship between expenditure and healthcare quality is not always linear. Austria combines high healthcare expenditure (11.2% of GDP) with one of the best healthcare systems in Europe (78.9). The Netherlands achieves the highest Healthcare Index score in the EU (81.5) while spending a lower share of GDP (9.8%) than Germany, France, Austria, or Sweden. Germany allocates 11.7% of GDP to healthcare – one of the highest levels globally – but ranks only 13th among EU countries according to the Healthcare Index (72.4). This demonstrates that institutional quality, management efficiency, prevention policies, digitalization, and workforce organization matter as much as funding levels.

The European picture reveals a clear geographical pattern. Northern and Western European countries dominate both healthcare quality and healthcare expenditure rankings, while Southern and Eastern European countries generally record weaker results. Countries such as Romania (56.5), Hungary (54.2), Malta (53.3), and Ireland (51.2) remain near the bottom of the Healthcare Index ranking despite different levels of spending.

The Balkan region remains significantly below the European average. North Macedonia (55.4) and Bosnia and Herzegovina (54.6) slightly outperform Serbia (52.1), while Albania (48.1) and Montenegro (47.4) record the lowest healthcare quality scores. Serbia’s position is particularly interesting because healthcare expenditure reaches 8.0% of GDP, exceeding the levels of Romania (5.7%), Hungary (6.4%), Croatia (7.1%), Poland (7.1%), Lithuania (7.3%), Estonia (7.5%), and Bulgaria (7.9%), yet healthcare quality remains comparatively low.

This suggests that Serbia’s challenge is increasingly one of efficiency rather than exclusively one of financing. The gap between healthcare spending and healthcare outcomes reflects broader structural issues related to governance quality, infrastructure modernization, healthcare management, demographic pressures, and the retention of medical professionals. The continuous outflow of doctors, nurses, and highly skilled healthcare workers reduces system capacity and increases pressure on remaining personnel, creating a cycle that negatively affects service quality and citizen satisfaction.

Particularly noteworthy is the close relationship between healthcare quality and demographic sustainability. Countries with stronger healthcare systems tend to achieve higher life expectancy, lower mortality rates, better management of chronic diseases, and greater resilience to population aging. As Europe faces demographic decline and labor shortages, healthcare quality increasingly becomes an economic competitiveness factor rather than merely a social policy objective.

The comparison between Serbia and the leading EU countries highlights a broader development challenge. The difference between Serbia (52.1) and the Netherlands (81.5) or Austria (78.9) cannot be explained solely by income levels or healthcare budgets. It also reflects differences in institutional capacity, investment efficiency, prevention policies, digitalization, management quality, and the ability to retain highly qualified professionals.

The lesson from European countries is clear – the countries with the best health systems are not necessarily those that spend the most, but those that spend the smartest. Health care is not a budgetary expense, but one of the most important investments a country can make. Therefore, the central challenge is no longer just increasing spending, but improving efficiency, governance, human capital retention and institutional performance. Countries that successfully transform health care spending into health care outcomes build not only healthier societies, but also more productive, resilient and competitive economies. For Serbia, health care is therefore not just a social issue – it is increasingly becoming a matter of a long-term development strategy.

Source: Numbeo; World Bank Database