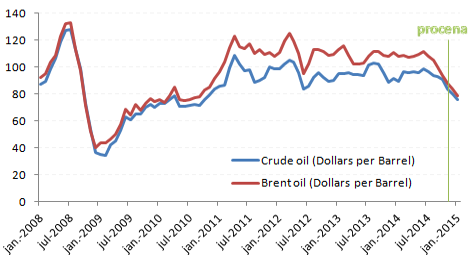

Nakon postepenog snižavanja cena nafte na svetskom tržištu tokom trećeg kvartala, početkom oktobra usledio dramatičan pad. Cena Brent nafte 14. oktobra pala je za čak 4$. Procena je da će na kraju godine pasti na 80$ po barelu. Očekivanja daljeg rasta posle junskog vrhunca od 115$ po barelu nisu se obistinila. Šta je to uticalo na promenu prognoza?

Svetska cena nafte je u postepenom padu od juna 2014. godine. Najveći zabeleženi pad je početkom oktobra. Brent nafta beleži pad cena, u odnosu na početak septembra od skoro 7$ po barelu, dok je laka nafta zabeležila pad od skoro 2$ po barelu. Očigledno je da je uzrok pada cena nafte slaba tražnja za naftom i/ili prevelika ponuda nafte. Slaba tražnja za naftom je posledica niskog rasta svetske ekonomije (otuda poslednja korekcija MMF i SB za rast svetske privrede u 2014. na 3,3%), pa neravnoteža na tržištu nafte (usled rastuće ponude) utiče na pad cene nafte.

Sve analize pokazuju da sa padom cene nafte na svetskom tržištu dolazi do rasta svetskog BDP-a. Prema analizi The Ekonomist pad cene nafte po barelu za 10$ dovodi do transfera 0,5% svetskog BDP-a od zemalja izvoznica nafte ka zemljama uvoznicama nafte. Postavlja se pitanje da li se može očekivati ovakav trend? Realno je da pad cena nafte može povećati potrošnju nafte u zemljama uvoznicama nafte (brzorastuće ekonomije i zemlje u razvoju), što doprinosi rastu svetskog BDP-a. Druge, pak, zemlje mogu iskoristiti manje izdatke za naftu za popunjavanje budžetskih rupa i vraćanje dugova, a ne za rast privrede. Trećima će uvozna inflacija dodatno pojačati deflatorne pritiske, sa recesionim efektima. Istovremeno, niže cene nafte mogu uticati na rast potrošnje razvijenih ekonomija, ali ostaje pitanje koji će efekat nadvladati. Svetski trendovi u trgovini su najvažniji faktor u kreiranju svetske cene nafte i njeni elementi ukazuju na smanjenje cena nafte. Smanjena je potražnja iz SAD, Japana i Evrope dok je povećana ponuda nafte iz zemalja van OPEC-a (Nigerija, Venecuela). I dalje je u Aziji najveća potrošnja nafte (Kina najveći pojedinačni uvoznik), pa se zemlje izvoznice nafte utrkuju koja će napraviti bolji aranžman. Međutim, tu su i brojni drugi faktori koje ne treba prenebregnuti, a koji su istovremeno uticali da se promene prognoze cena nafte do kraja godine (a i kasnije):

- rastuća tražnja inicirana špekulantima tokom juna (kriza na Bliskom istoku) i jula (značajan pad tražnje nafte od strane Japana);

- raste ponuda nafte (Libija i Iran povećavaju ponudu bez obzira na cenu jer im nedostaje gotovina, SAD rastom sopstvene proizvodnje nafte želi da smanji visoku uvoznu zavisnost);

- tražnja u opadanju (Japan od jula ponovo aktivirao nuklearna postrojenja);

- izostaje koordinirana akcija zemalja OPEC (tradicionalna uloga kontrolora svetske cene nafte nameće potrebu za zajedničkom akcijom usmerenu ka smanjenju obima proizvodnje nafte);

- povećanje zaliha kod razvijenih zemalja (utiče na smanjenje cena nafte, što je moguće izbeći samo manjom proizvodnjom nafte ili većom tražnjom za naftom nafte);

- dostignuća u nafti (retkost nafte prošlost – nove rezerve otkrivene u istočnom delu Mediteranskog mora, na Arktiku, u Severnom moru, zatim, Velika Britanija, Poljska, Brazil, Kina, Danska i dr. zemlje, sve veći izvori naftnih škriljaca – Rusija).

Svi napred pomenuti faktori uticaće na pad svetske cene nafte i u narednom periodu. Za sada zemlje OPEK-a mirno čekaju redovan sastanak zakazan za novembar 2014. (braniće 90$ po barelu). Neki izvori istuču da Rusija, prema svojim kalkulacijama, interveniše tek na nivou od 60$ po barelu. Potencijalnih nalazišta nafte je sve više, što ukazuje na dalje povećanje proizvodnje i ponude.

Regresiona analiza je pokazala da će potencijalno rastuća ponuda najviše uticati na pad cena u narednim mesecima. Očekivano niži rast svetske ekonomije (neminovna nova korekcija rasta na ispod 3%) vodiće nižoj tražnji za naftom, pa su izgledi da će cena nafte početkom 2015. godine (i Brenta i lake nafte) biti ispod 80$ po barelu. Rast tražnje za naftom može se očekivati tek u rastućoj fazi ekonomskog ciklusa, koja se predviđa za 2016. godinu. Do kraja 2014. godine usporeni rast brzorastućih ekonomija i ekonomija u nastajanju manje će doprineti, od očekivanog, rastu svetskog BDP-a (otuda korekcija). Za 2015. godinu taj doprinos neće biti dramatično veći. Dok se ne smanji proizvodnja i gomilanje zaliha nafte cene nafte na svetskom tržištu biće u padu.

After a gradual decline in oil prices on the global market during the third quarter, a dramatic drop followed in early October. On October 14, the price of Brent crude fell by as much as USD 4. It is estimated that by the end of the year the price will fall to USD 80 per barrel. Expectations of further price increases after the June peak of USD 115 per barrel did not materialize. What caused this shift in forecasts?

Global oil prices have been gradually declining since June 2014. The most significant drop was recorded in early October. Compared to early September, the price of Brent crude fell by nearly USD 7 per barrel, while light crude oil declined by almost USD 2 per barrel. It is evident that the main causes of the price decline are weak oil demand and/or excessive oil supply. Weak demand reflects low global economic growth (hence the latest IMF and World Bank downward revision of global growth for 2014 to 3.3%), while market imbalances driven by rising supply exert downward pressure on oil prices.

Most analyses indicate that falling global oil prices are associated with higher global GDP growth. According to The Economist, a USD 10 decline in the price of oil per barrel leads to a transfer of 0.5% of global GDP from oil-exporting to oil-importing countries. The question arises whether such a trend can be expected. Realistically, lower oil prices may increase oil consumption in importing countries (fast-growing and developing economies), thereby supporting global GDP growth. However, some countries may use lower oil expenditures to fill budget gaps or repay debt rather than stimulate growth. In others, imported deflation may intensify deflationary pressures, producing recessionary effects. At the same time, lower oil prices may boost consumption in advanced economies, but it remains unclear which effect will prevail.

Global trade trends are the most important factor shaping world oil prices, and current indicators point to further price declines. Demand from the United States, Japan, and Europe has weakened, while oil supply from non-OPEC countries (Nigeria, Venezuela) has increased. Asia remains the largest oil-consuming region, with China as the single largest importer, prompting oil-exporting countries to compete for more favorable arrangements. Nevertheless, several additional factors – often overlooked – have also contributed to revised oil price forecasts for the end of the year and beyond:

- rising demand driven by speculators in June (Middle East crisis) and July (a significant decline in Japan’s oil demand);

- increasing oil supply (Libya and Iran expanding production regardless of price due to liquidity shortages; the United States increasing domestic production to reduce import dependence);

- declining demand (Japan reactivated nuclear facilities starting in July);

- lack of coordinated action among OPEC countries (despite their traditional role as regulators of global oil prices, requiring joint action to reduce production);

- increased oil inventories in developed economies (putting downward pressure on prices unless offset by lower production or higher demand);

- technological and resource developments in oil (the perception of oil scarcity has faded—new reserves discovered in the Eastern Mediterranean, the Arctic, the North Sea; as well as in the UK, Poland, Brazil, China, Denmark, and others; expanding shale oil resources, particularly in Russia).

All of the above factors will continue to exert downward pressure on global oil prices in the coming period. For now, OPEC countries are awaiting their regular meeting scheduled for November 2014, aiming to defend a price level of USD 90 per barrel. Some sources suggest that Russia would intervene only if prices fall to around USD 60 per barrel. The growing number of potential oil fields points to further increases in production and supply.

Regression analysis indicates that rising supply will be the dominant factor driving price declines in the coming months. Slower global economic growth (with an inevitable further downward revision to below 3%) will reduce oil demand, making it likely that oil prices (both Brent and light crude) will fall below USD 80 per barrel in early 2015. A meaningful increase in oil demand can be expected only during an expansionary phase of the economic cycle, projected for 2016. By the end of 2014, slower growth in fast-growing and emerging economies will contribute less to global GDP growth than expected (hence the revisions), and this contribution is unlikely to increase significantly in 2015. Until oil production and inventory accumulation are reduced, global oil prices will remain under downward pressure.